CFDs are leveraged products that incur a high level of risk. Know more

- Accounts

Trading DetailsCFI AIHelp & Support

Trading DetailsCFI AIHelp & Support

Introduction To Financial Markets

What is options trading?

August 1, 2024

What are Options

Options contracts, or simply options, are agreements that give the holder the right, but not the obligation, to buy or sell a specific amount of an underlying security at a specified price at or until a defined time in the future. Options are derivative instruments because their value depends on the value of their underlying asset. Further, options are “decaying” or “wasting” assets because, all other things being equal, their value will decline over time until they expire. All assets depend on some definition of value, which is then modified by supply and demand factors established by buyers and sellers. However, options depend on many other variables, the most notable being their strike prices and the time left until they expire.

Benefits of Options Investing

There are two major benefits for options investors. The first is leverage, or the ability to gain price exposure to a given amount of assets for a lower initial cost. The second is hedging a position in the spot market. For a small premium, the options investor has the right to buy or sell an asset at a specific price. They will have to pay that full price (or deliver the full amount of assets) at some time in the future but they can choose to close out their position before that happens. Therefore, they can profit from the move in the underlying asset for a lower cost, and therefore lower risk.

Options Terminology

- Call option: A call gives the holder the right, but not the obligation, to buy a defined amount of the underlying security at a certain price at or by a certain date.

- Put option: A put gives the holder the right, but not the obligation, to sell a defined amount of the underlying security at a certain price at or by a certain date.

- Strike price: This is the price at which the holder of the option may buy or sell the underlying security. For example, a call option with a strike price of 50 gives the holder the right to buy the underlying stock at that price no matter what the price of the stock may be at that time.

- Expiration: The date at which the option holder no longer has any rights and the option no longer has value.

- Premium: The price paid for the option.

- Open interest: The number of options contracts outstanding per strike/expiration combination.

- Exercise: Using the rights acquired under the option to buy or sell the underlying security.

- In-the-money: A call option with a strike price below the price of the underlying; a put option with a strike price above the price of the underlying.

- Out-of-the-money: A call option with a strike price above the price of the underlying; a put option with a strike price below the price of the underlying.

- At-the-money: An option with a strike price at or very close to the price of the underlying.

- American style: Options that may be exercised at any time up to and including their expiration date.

- European style: Options that may be exercised only at expiration.

Reasons for Trading Options

There are many reasons why an investor or trader trades options. The main reasons, as with other derivatives markets, are to hedge another position or to speculate on the performance of the underlying security.

- Hedging: A hedge is like an insurance policy, in that it can help to mitigate risk for a small fee. For example, a portfolio manager buys a large position in Company A stock for its long-term price appreciation potential but is worried that the next earnings report will show short-term issues.

- Speculation: Options allow both buyers and sellers to capitalize on their market forecasts, whether they are bullish, bearish, or neutral. However, because options prices depend on many factors, including market volatility, traders can profit from increases or decreases in those factors as well.

Measuring Options Sensitivities

Options analysts also look at derivatives of the price that measure how fast their prices decay over time, how fast their prices change with a given change in the price of the underlying and more. These derivatives are designated with Greek letters such as delta and gamma, so options traders simply call them “the Greeks.”

◾ Delta

Measures how much an option price changes for a one-point move in the underlying. Its value ranges between 0 and 1 for calls and between –1 and 0 for puts.

◾ Gamma

Measures the rate of change in delta. It is essentially the second derivative of price. Values are highest for at-the-money options and smallest for that far in- or out-of-the-money.

◾ Vega

Measures the risk from changes in implied volatility. Higher volatility makes options more expensive since there is a greater chance that the underlying security price will move above the strike price for a call, or below the strike price for a put.

◾ Theta

Measures the rate of time value decay and it is always a negative number as time moves in only one direction.

◾ Rho

Measures the impact of changes in interest rates on an option’s price. Since interest rates do not change very frequently, this Greek does not get the same exposure as the others.

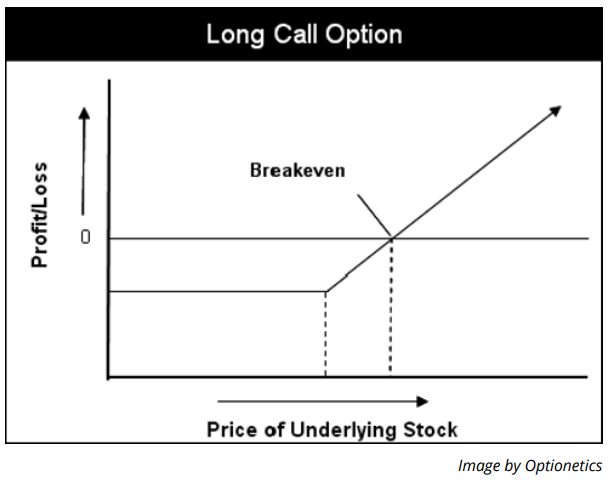

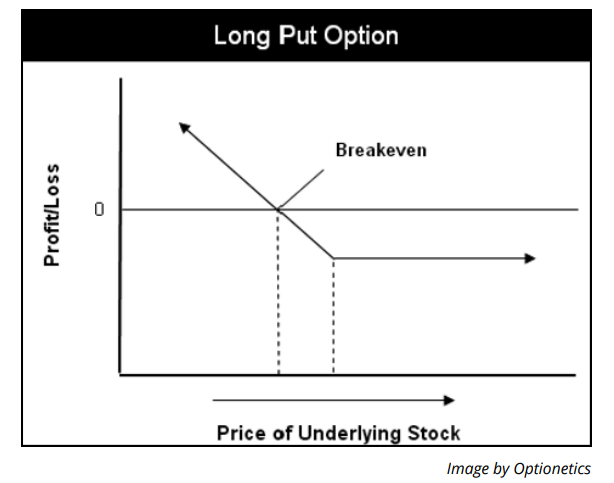

Profiling option trades with risk graphs

Basic call and put option risk graphs are slightly different than stock risk graphs because they incorporate the risk and reward for the security, along with the breakeven level. Position-specific profiles will include stock prices on the x-axis and profits/losses on the y-axis.

A basic call options risk graph is similar to a long stock risk graph, with two important distinctions: You need to account for the call option premium at the breakeven level. Your losses are capped to the downside before a stock declines to zero. The potential risk for a call option is limited, whereas the potential rewards are unlimited.

basic put option risk graph is similar to a short stock risk graph, with a couple of distinctions. The second one is extremely valuable if you’re bearish on a stock and things go against you. You need to account for the influence of the time value surcharge on the put option’s premium at the breakeven level. Your losses are capped to the upside and are therefore limited. The potential risk for a put option is limited, whereas the potential rewards are limited but high. As is the case with calls, put options can lose 100% of their value, while the loss as measured in dollars is always less than what you may lose in a stock.

Disclaimer: The content published above has been prepared by CFI for informational purposes only and should not be considered as investment advice. Any view expressed does not constitute a personal recommendation or solicitation to buy or sell. The information provided does not have regard to the specific investment objectives, financial situation, and needs of any specific person who may receive it, and is not held out as independent investment research and may have been acted upon by persons connected with CFI. Market data is derived from independent sources believed to be reliable, however, CFI makes no guarantee of its accuracy or completeness, and accepts no responsibility for any consequence of its use by recipients.

Related Articles

See All